Those who remember 2008 will know that second-order effects can prove just as destructive as the immediate shock of a financial crisis.

Much has been said about the ongoing turmoil in oil and natural gas markets this week, but now a new subprime-type crisis, high-risk loans, may also be added, leading to a combination of the situation at the end of the 2000s with the oil shock of 1973.

This is an entirely realistic scenario.

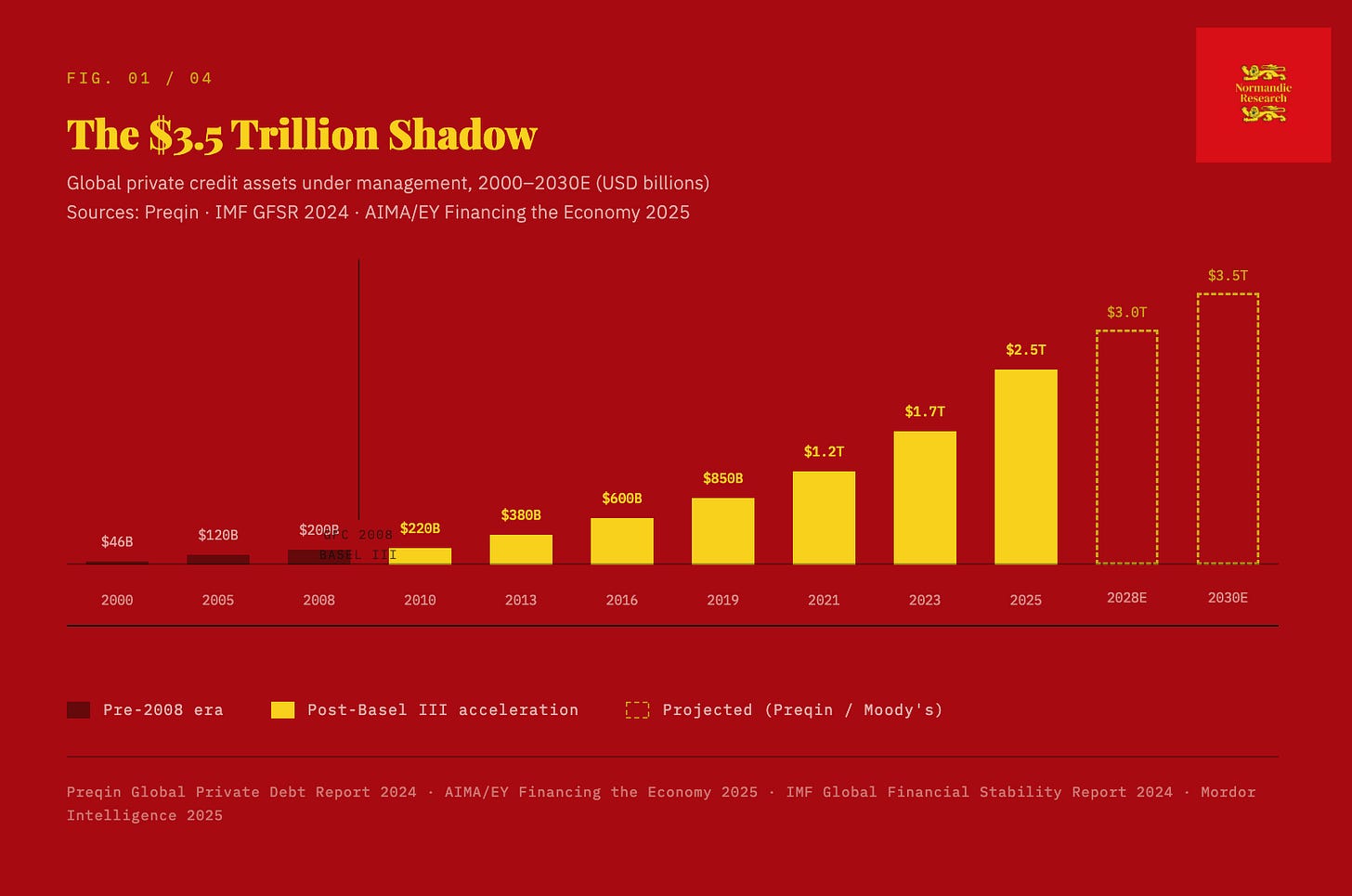

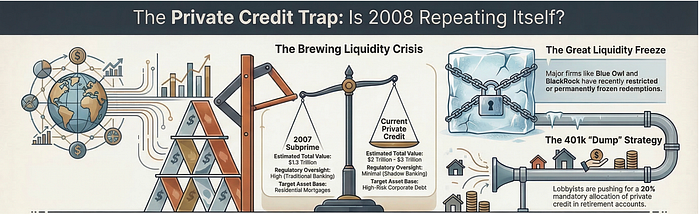

The “subprime” crisis of the present era is private credit, a market estimated at $2–3 trillion, larger in nominal terms than the subprime mortgage market 20 years ago.

Bloomberg reported this week that JPMorgan and Goldman Sachs began offering hedge funds the ability to short private credit.

The two banks have created “baskets” of listed companies with exposure to this market.

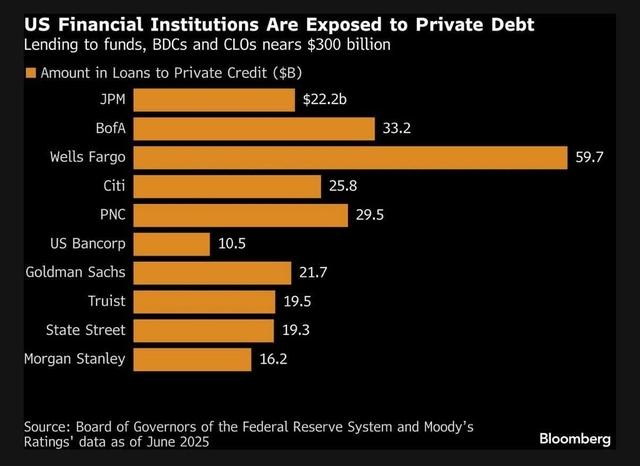

As two decades ago, European financial institutions are among those with exposure to the riskiest segment of the market.

In the 2000s, the recipient of this risk was the infamous “naive banker of Düsseldorf”.

Today, it is clear that the institutions involved have significant exposure to software companies.

This is a sector that is among those most affected by artificial intelligence, which has highlighted the unsustainability of the “software-as-a-service” model.

Financial crises arise from vortices of developments that interact.

This particular “bubble” is not going to burst immediately, such phenomena usually last for a long time before manifesting.

JPMorgan, for example, has already begun reducing its private credit portfolio, amounting to $27 billion, since September.

At the same time, investors have begun submitting redemption requests from funds managed by private entities.

Here the core problem of seeking returns outside organized markets emerges, when panic breaks out, everyone seeks to exit simultaneously and fund managers are forced to impose restrictions on redemptions.

The hedging strategy is based on total return swaps, financial instruments that separate the ownership of an asset from its cash flows.

As with the famous credit default swaps of the financial crisis, bets are made through synthetic versions.

For those not familiar with these complex instruments, the idea was characteristically depicted in the casino scene of the movie The Big Short, where a player bets at a blackjack table and others begin to bet on his hand, creating a chain.

Credit “bubbles” evolve in successive stages.

Synthetic DOs, collateralized debt obligations, constituted a secondary phenomenon before the collapse of the previous crisis.

Today, we may be facing a similar process.

What is happening with the “bubble” in private credit

For years it has been known that the “buy now, pay later” sector, BNPL, is based on particularly fragile foundations.

The main problem has always been the quality of the loans.

The entire business model revolves around the immediate provision of credit with minimal creditworthiness checks, to consumers making small purchases.

Companies whose main “innovation” is that they allow consumers to repay a $40 online purchase in four installments hardly appeal to the most creditworthy audience.

On the contrary, the model almost guarantees the opposite.

When financial companies create products that facilitate the financing of extremely small, optional expenses, they essentially target borrowers either without sufficient liquidity for immediate payment or with already exhausted more traditional borrowing means.

When consumers put even everyday purchases into installments, the pool of borrowers is far from being considered “prime”.

The same dynamic has been visible for years in peer-to-peer lending and fintech credit.

Platforms such as Affirm, as well as payment ecosystems linked to companies such as Block, built impressive success stories by expanding access to credit to individuals who historically did not meet the criteria of traditional products.

For a time, this appeared as financial innovation, especially as long as there were willing buyers for the loans.

In reality, it was mainly an expansion of unsecured credit to lower credit-quality segments.

The liquidity created by central banks

This approach worked extremely well in a zero-interest-rate environment, where capital was abundant and investors were seeking returns.

It also worked during the three-year period of the Covid pandemic, when liquidity from the Federal Reserve was essentially unlimited.

However, it becomes far less impressive when interest rates rise and credit markets begin to operate again under stricter conditions. In reality, we are now seeing the “trick” that was labeled innovation being revealed, first in companies such as Carvana, then in private credit, and now in BNPL.

Low-credit-quality lending and accounting maneuvers do not constitute innovation, no matter how much they are “beautified”.

The most recent example comes from a report by the Wall Street Journal, which describes pressures on a private credit fund managed by Stone Ridge Asset Management.

The company manages the Stone Ridge Alternative Lending Risk Premium Fund, known as LENDX, which invests in loans and securities linked to fintech loans.

Sorry, we cannot return your funds

These include BNPL loans from Affirm, as well as personal loans from LendingClub and Upstart.

The portfolio also includes financing through payment platforms such as Block and Stripe.

Recently, investors in the fund attempted to withdraw capital far greater than what its structure allows. Stone Ridge informed that it can satisfy only about 11% of redemption requests.

The fund is of the “interval” type, which means that investors cannot exit at any time, but only during specific time windows, with a limited percentage of share repurchases per quarter.

This model works as long as investors remain calm.

The problem arises when many wish to exit at the same time. The underlying loans are illiquid and cannot be sold quickly without significant losses, so the easiest solution is to restrict withdrawals.

None of this is particularly unexpected.

For years it has been pointed out that fintech platforms grant loans to individuals who traditionally would not meet the criteria for bank lending.

Banks avoided these borrowers for a simple reason, when economic conditions deteriorate, default rates rise rapidly among the weakest.

The fintech model did not eliminate this dynamic, it merely postponed it as long as capital markets financed the expansion.

The broader private credit market is also beginning to show signs of pressure.

In recent periods, funds linked to major managers such as Morgan Stanley, BlackRock, and Cliffwater have restricted withdrawals due to increased requests.

Concern was recently reinforced by statements from John Zito of Apollo Global Management, who warned that many assets in the private market are valued at levels that do not reflect current economic conditions.

In particular, private equity deals in the period 2018–2022, especially in the software sector, were made at valuations significantly higher than comparable listed companies. In case of problems, loan recoveries may be limited to 20%–40% of value.

All this is happening while the economy is beginning to feel the effects of real positive interest rates.

For much of the previous decade, credit markets operated with almost zero cost of money, allowing questionable lending models to flourish.

With rising interest rates and tightening liquidity, loan quality is once again becoming important.

The turn of the credit cycle

The combination of pressures in BNPL and increasing redemption requests in private credit is an indication that the credit cycle has turned.

Nevertheless, investors still appear relatively comfortable with companies such as Blue Owl Capital and Ares Management, as well as with the broader universe of BDCs, BNPL lenders, and certain regional banks with significant exposure to the sector.

Pressures are expected to intensify in both BNPL and private credit, as the effects of higher interest rates spread through the system.

One sector that could be affected next is commercial real estate, where valuations still appear optimistic under the current financing environment.

Ultimately, the Federal Reserve is very likely to intervene if the situation deteriorates significantly, creating some form of liquidity support mechanism. However, historically, such interventions come after a period of forced deleveraging has already occurred.

If this process has already begun in fintech financing and private credit, then the unpleasant phase, where investors reassess the real value of assets, is likely still ahead of us.

And this is usually the most difficult phase for everyone and blood is expected to be spilled.

www.bankingnews.gr

Σχόλια αναγνωστών